Worst year since 2008 but some optimism returns to global investment markets

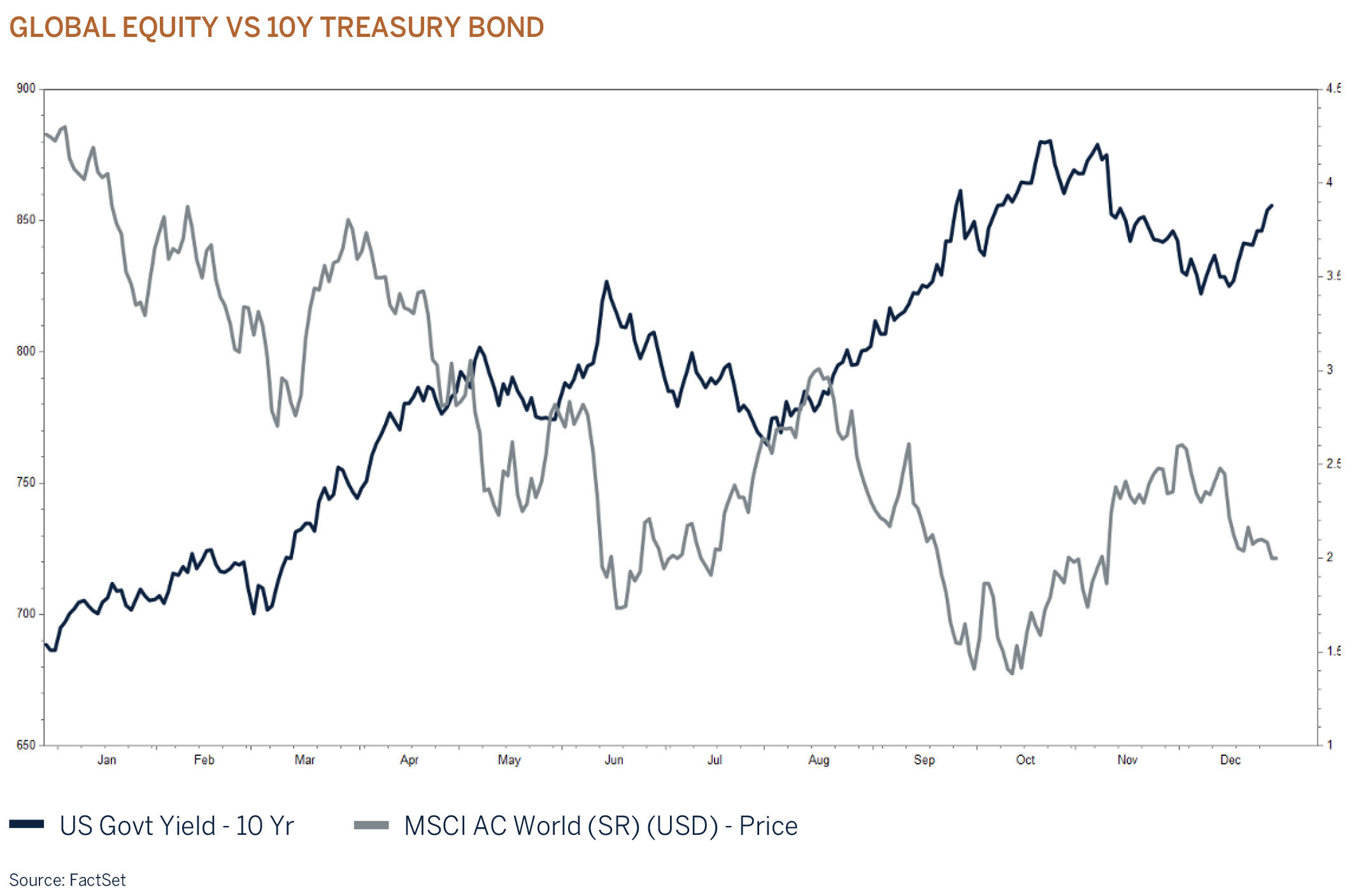

Despite global central banks best efforts to rein in inflation by way of slowing demand growth with much tighter monetary policy, risk assets made a comeback during the fourth quarter of 2022 whilst the US greenback lost its shine, giving back some of its significant outperformance over the past year. Several factors contributed to the bounce from the October lows with investors focusing on the improved outlook for inflation as consumer goods, food and energy prices all eased leading to predictions that inflation has peaked. An important development, as high and stubborn inflation coupled with a vibrant labour market, has resulted in one of the most aggressive interest rate hiking cycles in recent history. With the disinflationary trend intact as supply constraints ease, central banks have indicated their preference to slowdown the pace of monetary tightening and to follow a “wait and see approach”, meaning that interest rates will probably peak towards the end of the first quarter in 2023. Additional factors that contributed to the bounce in equity markets are the prospect of less restrictive COVID-19 measures in China and a significant decline in the price of natural gas in Europe. Gas storage levels have been adequately increased to cater for the colder winter months in the Northern hemisphere as users switched to liquid natural gas. As a result, and not for the first time this year, we have seen that a lower than expected inflation print in the US has resulted in lower bond yields and a rerating in equity markets, an indication of just how sensitive equity valuations and risk appetite have become to changes in the outlook for the cost of funding (bond yields).

Interest rates have increased significantly over a short period and are not expected to come down from the current restrictive level any time soon, given that inflation by any standard remains much too high. The outlook for macroeconomic conditions, monetary policy and the geopolitical backdrop remains highly uncertain given the warning from US Federal Reserve Chair Powell that “monetary policy affects the economy and inflation with uncertain lags, and the full effects of our rapid tightening so far are yet to be felt” and as such investors should expect volatility to remain elevated and very much data dependent as the global economy enters a period of below-trend growth or, even worse, a recession. We have reduced risk in offshore portfolios further by cutting the equity exposure to underweight and have used the proceeds to increase the allocation to fixed income to neutral, thereby locking into higher yields. Although equity valuations are much more reasonably priced than a year ago when interest rates were exceptionally low, the recent rally leaves investors with a limited margin of safety should corporate profit margins and/or earnings decline, as we expect.

China – awakening from the COVID-19 restrictions

While COVID-19 cases have been increasing at an alarming rate in mainland China and Hong Kong, authorities have indicated their willingness to start relaxing some of the draconian restriction measures in place. The stock market has rebounded strongly from its lows on this news and globally, sectors such as resources and mining stocks have benefitted the most on hopes of a recovery in final demand as China’s economy awakens once more.

The Chinese economy undershot expectations in 2022 due to the enforcement of COVID-19 related lockdowns coupled with a slowdown in the property market as many real estate developers encountered liquidity and solvency difficulties as funding became challenging. Lower property prices, a weakening economy and large-scale layoffs resulted in investors and banks taking a more cautious approach towards injecting more capital into the real estate sector. A weakening real estate sector poses significant risks to local governments that have previously relied on proceeds from the selling and letting of land.

The Chinese authorities are aware of the negative spillover effects to the rest of the economy as the housing/property market and related industries contribute almost 50% to the economy. The initial softening in the property market was expected as the Chinese government implemented measures to cool-off rapidly rising property prices, which became a major concern for households looking to enter the market for the first time. In addition, Chinese authorities became progressively concerned about the increasing levels of speculation and size of the industry. Their challenge at present is to prevent the housing market from collapsing further and they are injecting liquidity and reducing some of the restrictions on individuals/households looking to enter the market. The Japanese experience of a “lost decade” and persistent deflation due to the collapse of the property bubble is something that the Chinese government will be hoping to avoid.

The path of economic recovery will likely be bumpy and the timing of the lifting of COVID-19 restrictions may be questionable before the Chinese New Year celebrations over January/February, given the already increasing levels of infection rates. However, with the assistance of lower interest rates and a liquidity injection, 2023 should be a year of recovery for one of the largest economies in the world, with positive implications for countries and regions dependent on China’s fortunes.

Equity markets – ongoing volatility in H1 2023 likely

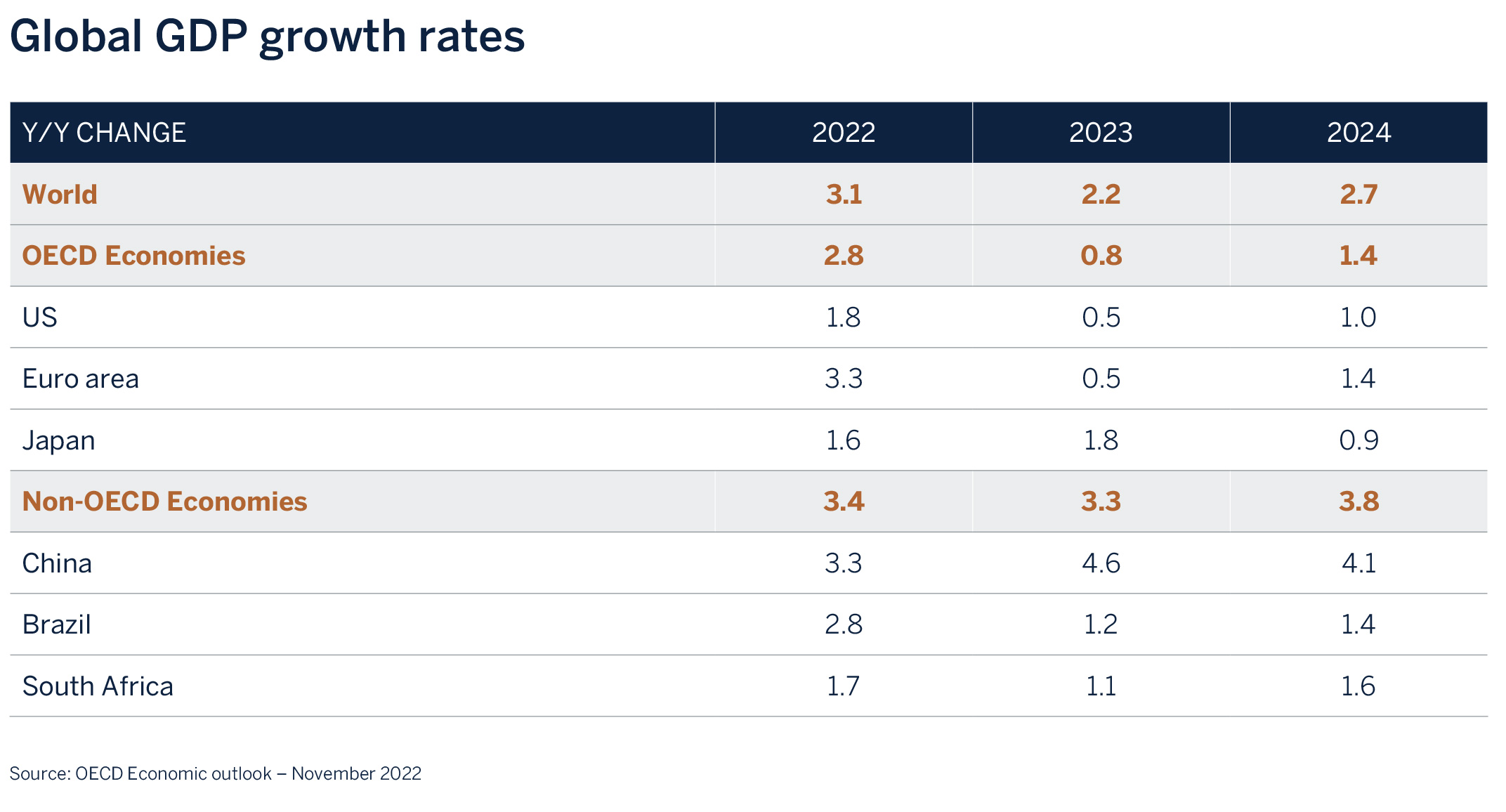

The impact of higher interest rates coupled with lower real disposable household income on the global economy can be seen in the table below as the world enters a phase of below trend growth driven by an expected sharp roll-over in the US and the Euro area’s credit cycle and a slowdown in private sector fixed investment. The full effects of the aggressive monetary tightening seen in 2022 are still to be felt. It just takes time!

Equity valuations have already meaningfully responded to the weaker economic and higher interest rate outlook with valuation multiples declining sharply during 2022 as share prices fell. Indeed, fixed income assets also performed very poorly as interest rates have been raised to fight inflation which is seen as a worse evil than short term lower economic growth. The upshot is that for the first time in many years, non-equity (cash and fixed income) assets have once again become a viable investment option (given higher yields) to consider from a diversification perspective. Equity valuations are much more reasonable today than what they were a year ago and are trading in line with long term averages. But the economic and geopolitical outlook remains uncertain, and equities are not yet priced for a worse than expected economic and/or earnings growth outlook. Consensus expects positive earnings growth for this year, but that would appear to be too optimistic in an environment of subpar economic growth.

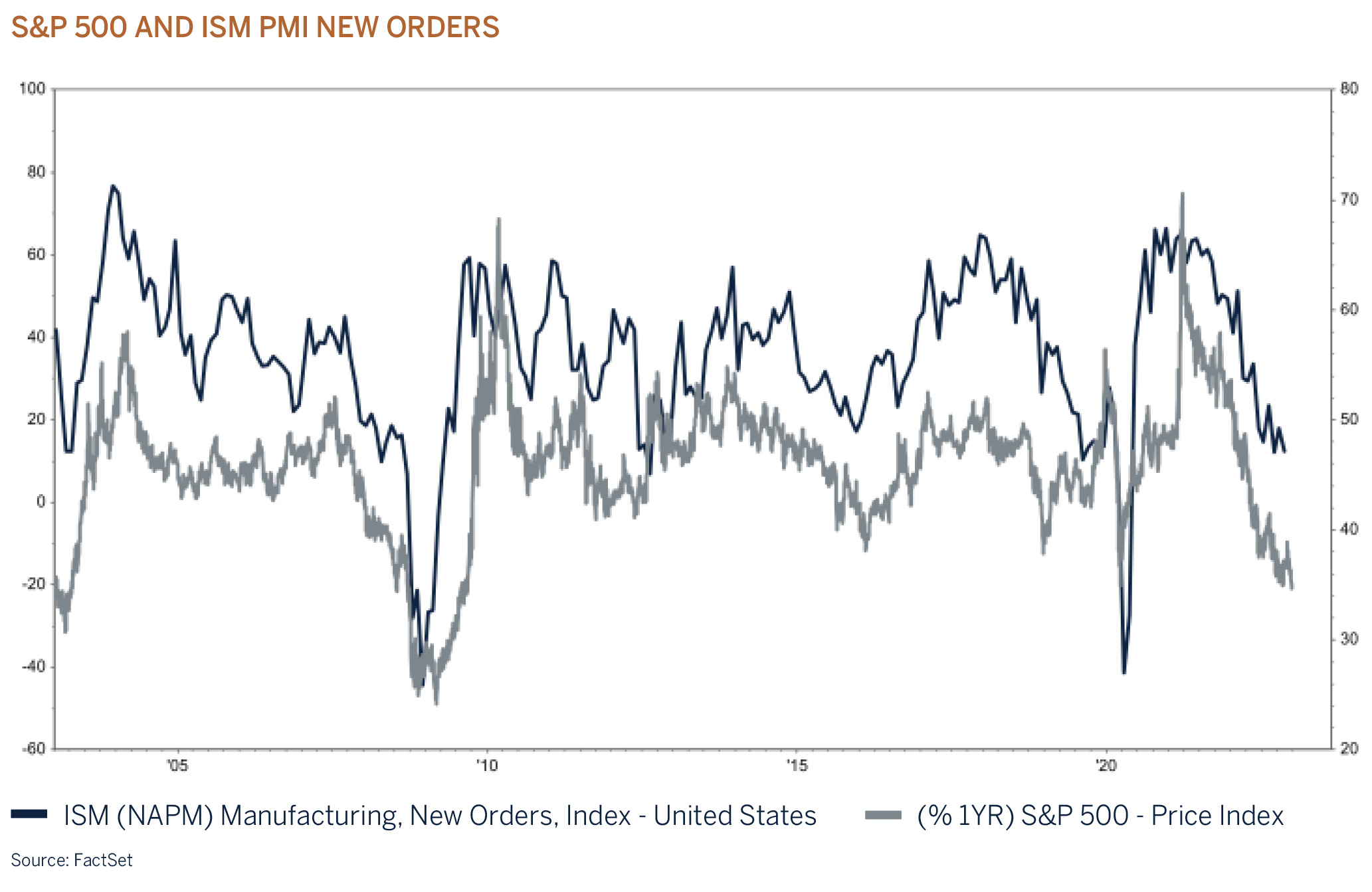

Leading economic indicators turning lower

In the near term, risks are tilted to the downside as corporates, investors and households adapt to an environment of higher interest rates and costs, and leading indicators are pointing to a cyclical slowdown and recessions in several western world economies. Given the ongoing challenging near-term outlook we have taken a more cautious (tactical) stance in the short term and will continue to actively monitor the key drivers of equity returns, which include valuations, the outlook for inflation and interest rates, the change in direction of leading economic indicators and developments in employment. We stand ready to change tack as the environment dictates.

US Dollar

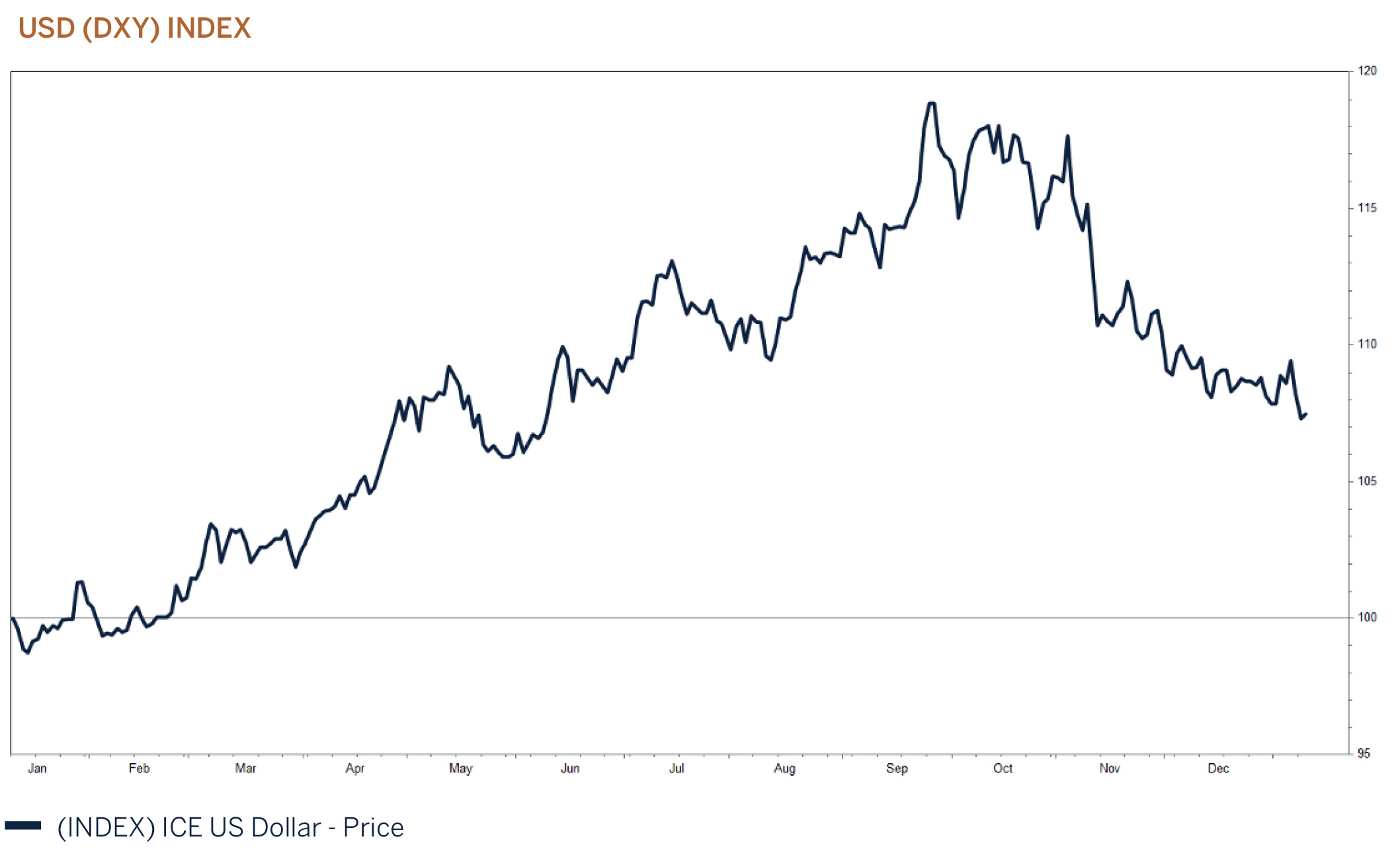

Expectations that inflation has peaked and therefore, the US tightening cycle is closing in on terminal rates weighed on the US Dollar in the fourth quarter. The currency’s significant rally over previous quarters, which defied even our bullish expectations, left it vulnerable to a retracement which doesn’t surprise us. Despite this sell off, the currency as measured by the DXY Index was still the standout winner of 2022 appreciating +8.21%, adding to a strong gain of +6.37% the previous year.

Recent weakness has prompted many to reassess their outlooks to negative for the year ahead and whilst we are cognisant that the US Dollar’s peak may be behind us, given the mixed outlook for global growth, it is perhaps premature to expect the currency to continue to weaken at the same pace as recorded in the past quarter. Many factors that have supported the currency throughout its rally remain in situ. Namely, the US economy maintains a distinct economic growth advantage over counterparts such as Europe (including the UK) which should ensure an ongoing interest rate and yield advantage. Reserve currency status has been beneficial throughout recent quarters of ‘risk-off’ volatility and this theme remains in play as global central banks continue to tighten policy and therefore, recession risks rise.

An eventful year

The year 2022 can best be described as a very difficult year, characterised by extreme volatility, with no asset class spared. On the morning of 24th February 2022, Russian President Vladimir Putin announced a “special military operation” seeking the “demilitarisation” and “denazification” of Ukraine. This still raging war, with no end in sight, has been the major source of market volatility throughout the year. The war has been the major driver of global inflation with central banks forced to aggressively hike interest rates in response to runaway inflation in their respective economies. South Africa was not shielded from this spiraling inflation and in response, the South African Reserve Bank (SARB) hiked rates by a cumulative 325 basis points during the year.

South Africa’s specific risk factors added to volatility in the year. In the second quarter the economy, as measured by GDP, contracted by 0,7% with the manufacturing sector being the largest detractor. This sector was negatively impacted by the floods experienced in KwaZulu Natal during this period. South Africa’s potential grey listing by the Financial Action Task Force (FATF), a global money laundering and terrorist financing watchdog, added to the volatility during the second half of the year. In October 2021, South Africa was given a 12-month window to address the high use of cash, address skills and capacity issues in state security and law enforcement agencies, improve the monitoring of cross border flows and enhance beneficial ownership visibility. South Africa may be added to the grey list in February 2023, should the FATF not be satisfied with the progress the country has made in this regard.

Loadshedding has become a major obstacle to South Africa’s economic growth outlook, with the country in 2022 experiencing the highest frequency of rationed electricity in its history. The challenges that come with stabilising the power utility and providing a reliable power supply have cost the head of yet another executive, with the current Group Chief Executive announcing his resignation in December. Whoever the shareholder appoints to succeed the incumbent, that person, it seems will be inheriting a poisoned chalice, with the power utility having been led by no less than ten Chief Executives in the last decade.

Despite lackluster growth, annual inflation rose to 7,8% y/y in July, the highest in thirteen years and has since decelerated to 7,2% y/y. We expect inflation to continue to soften from these levels, given the recent decline in global energy and food prices. The SARB still considers risks to inflation tilted to the upside and emphasised the data dependence of future interest rate decisions. The central bank is still of the view that it is not ahead of the curve in its interest rate decisions and more hikes are expected during the first half of this year.

The year would not have been complete without a feature from domestic politics and its contribution to volatility. In early December, a three-person panel chaired by a former Chief Justice and commissioned by the National Assembly tabled its final report. The panel had been asked to investigate if the President of the Republic had committed an impeachable offence around allegations of concealment of theft of foreign currency at his game farm, Phala Phala. The panel found that the President had a case to answer, and it was up to the National Assembly to adopt the report and pursue the matter further. In the days that followed, with the President reportedly prepared to resign over this report, currency and domestic bond yields were sent into orbit, with the currency weakening to above R18,00/USD and bond yields above 11,50%. In the end the ruling party rallied around its politically embattled President and talked him out of resigning and advised him to take the report on judicial review. The ruling party also used its majority in the National Assembly not to adopt the report. As a result, the President lived to fight another day and subsequently went on to win his second term as the leader of his party, the ruling African National Congress. Consequently, the currency and bond markets breathed a sigh of relief with the local currency ending the year below R17,00/USD and bond yields rallying by more than 70 basis points to end the year trading below 10,80%.

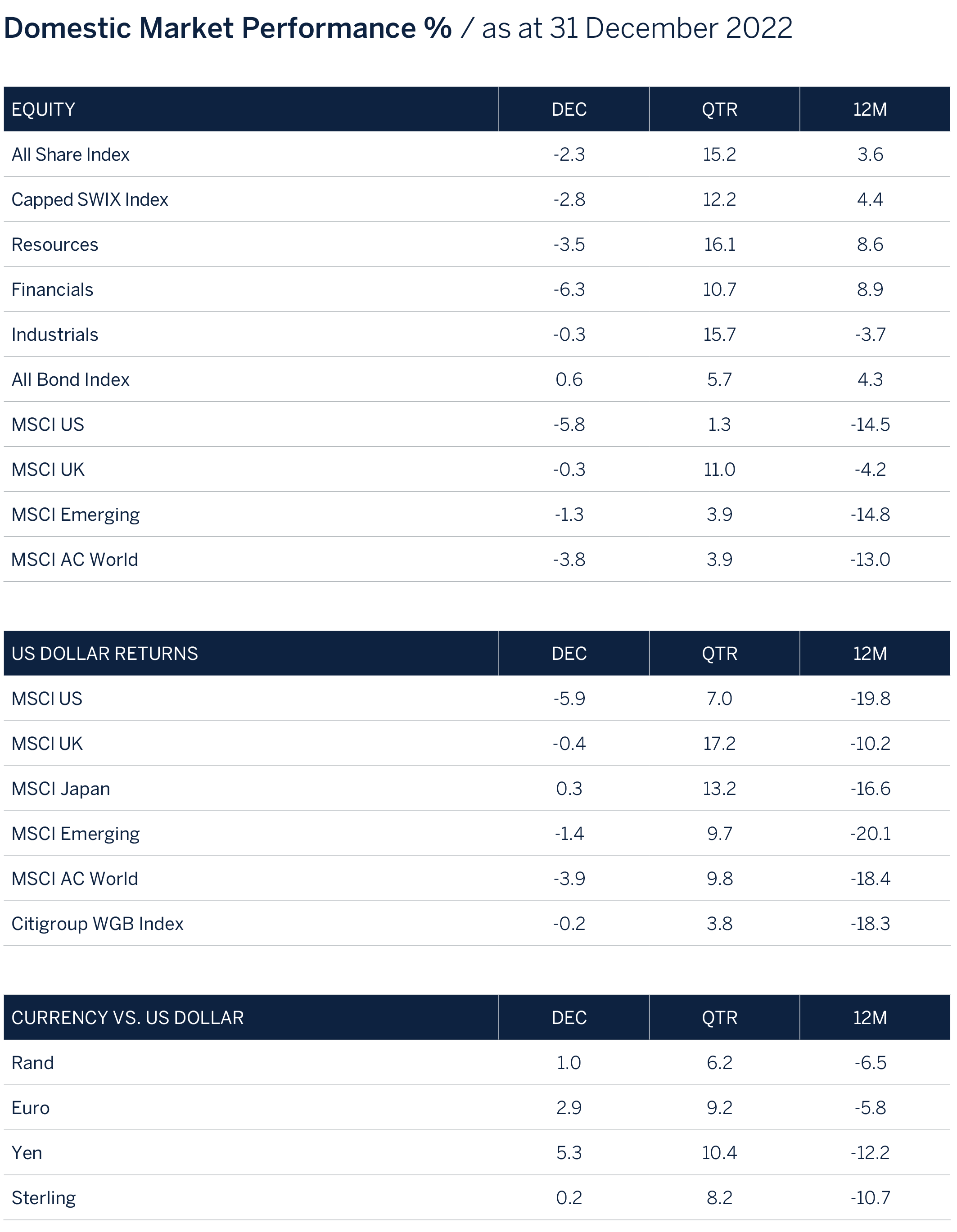

Investment returns

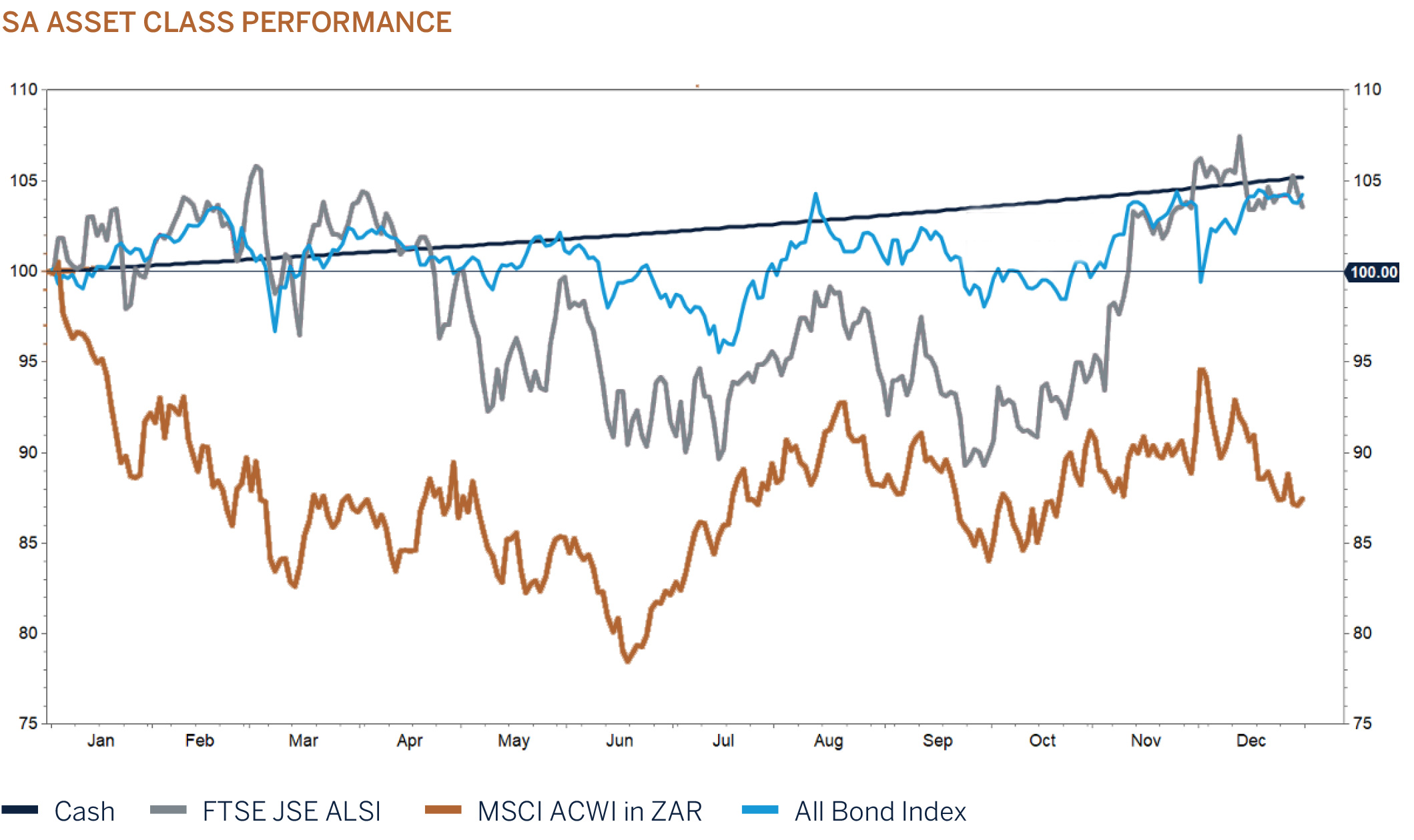

South Africa’s investment markets have benefitted from the change in global sentiment and the expectation of a reopening of China’s economy. During the fourth quarter local shares as measured by the JSE All Share Index generated a positive return of 15%, resulting in the local bourse outperforming Global and Emerging Markets handsomely during 2022. And while fixed income assets in developed markets experienced their worse year in memory, – 12.9% (ZAR), South African government bonds returned a positive 4.3%. The result is that South Africa’s equity and bond indices have outperformed global investment markets over the past 3 years. A remarkable achievement, given how poorly the domestic economy has performed, and perhaps an illustration of the relative cheapness of South African assets when compared to developed and emerging markets over the same period.

It is interesting however to note that many of the stocks that had performed well over the past few years have very little to do with the fortunes of SA, given that the outperformance was primarily driven by Resources (higher commodity prices), Information Technology (Naspers/Prosus/Tencent) and dual listed stocks such as Richemont. This is best illustrated by looking at the performance of the MSCI South African Equity Index which excludes all dual listed shares from the local market. As can be seen from the chart below, when measured in US Dollars, that the index has not delivered a positive return since 2007. This is both an unfortunate and sobering reflection of how SA corporates have fared over this period and is a strong argument why investors should seek to diversify their wealth internationally.

Economic reforms gaining traction

We have previously written about the important role that Operation Vulindlela plays in driving the much-needed economic reforms in South Africa. It has been two years since President Ramaphosa announced the establishment of Operation Vulindlela to drive a far-reaching economic reform agenda for South Africa to shift the country’s economic growth trajectory and enable investment and job creation. As a reminder, “the primary role of Operation Vulindlela is to monitor progress on priority reforms and provide support where necessary to accelerate their implementation” and the ultimate goal of the structural reforms, is to enhance the operating environment and lower the costs of doing business, so that firms invest and grow the productive capacity of the economy.

And while most South African’s were troubled by another bout of increased loadshedding over the festive season and Andre de Ruyter’s “unexpected” resignation from Eskom, National Treasury released a report on the progress and achievement of Operation Vulindlela, which provides a glimmer of hope to SA’s struggling economy over the medium term. National Treasury estimates that the cumulative benefit to the economy could be as high as R438bn should the reforms be successfully implemented by 2030. It is also encouraging that private sector involvement has once again been identified and highlighted as key in achieving government’s growth ambitions.

Several new reform objectives have been identified and added to the list: Creating an appropriate legislative framework for hemp & cannabis Enabling the devolution of passenger rail functions to local government Titling reforms for low-cost housing and The development of a fit-for-purpose procurement regime for state-owned entities.

The update suggests progress on some areas, but ongoing implementation challenges for a number of key reform goals, particularly in the areas of energy and water. Overall, the update suggests that the reform programme is grinding forward, even though of the 35 reform goals only 7 have been completed while 5 are judged to be on track.

For Q3 22, the NT’s update listed the following particular OV achievements:

The government issued RFPs for private sector participation in the container operations at the Ports of Durban and Ngqura (Port Elizabeth), with partners to be identified by the end of January

Agreements on 6 renewable energy projects amounting to 784MW from Bid Window 5 have been signed (though the remaining 1,816MW of projects in Bid Window 5 are struggling to reach financial closure)

The envisaged amount of renewable energy to be procured through Bid Window 6 was lifted from 2,600MW to 4,200MW

A draft amendment to Schedule 2 of the Electricity Regulation Act to remove the 100MW licensing threshold for private generation was published (and further progress on this front was secured in Q4 when Minister Mantashe gazetted the changes in mid-December)

The National Water Resources Infrastructure Agency Bill and revised Raw Water Pricing Strategy were released for a 90-day public consultation period (just ended); and

Processing of work visa applications was returned to South Africa’s embassies abroad (to speed up processing time)

The NT’s update also highlights what can be expected in the way of further reforms by the end of this fiscal year, including:

Establish a feed-in tariff and tax incentives for residential rooftop solar

Establish a ‘one stop shop’ for all energy projects

Appoint an independent board to operationalise the independent transmission entity

Table the Electricity Regulation Act amendment bill in Parliament

Complete the migration of households to digital, with the switch off of analogue broadcasting by the end of March

Private partnerships in place for Durban and Ngqura ports by January 2023

Announce further container freight rail slots for sale, using the lessons of relatively unsuccessful first auction attempts

Table the National Water Resources Infrastructure Agency Bill in Parliament

Establish a steering committee on low-income housing titles to begin clearing the big backlog

COVID-19, the infighting within the ANC, lack of political will, and a shortage of relevant skills and experience, have contributed to the slow rate of progress. But now that Ramaphosa’s leadership within the ANC has been confirmed and strengthened at December’s ANC election conference, we would expect a renewed focus from the President to tackle the job at hand and drive the necessary changes required to remove bureaucratic red tape and corruption, while ensuring that many of the suggested reforms are implemented successfully. Execution risks remain and investors should not expect much improvement in economic activity in the near term. If some of these reforms are successfully implemented and the private sector is encouraged to participate, SA’s growth trajectory stands to benefit to such an extent that it would encourage an inflow of investment while at the same time alleviate poverty.

Conclusion

2022 was a year that most investors would like to forget. Prices of equity and fixed income assets declined sharply after global central banks changed course to combat inflation. The war in Ukraine was supposed to be short lived and so too were the COVID-19 restrictions in China. Valuations across asset classes have adjusted to the reality that both inflation and interest rates will remain stickier than what was expected a year ago. Volatility and cheaper valuations do however provide new opportunities that should be welcomed by patient investors that focus on long term fundamentals. Many high-quality stocks with structural growth tailwinds and strong balance sheets have become attractive once again and provide the necessary margin of safety for us to consider in client portfolios. Cash and fixed income yields have also adjusted significantly higher and are providing returns that exceed longer term inflation forecasts, which allows investors to take less risk (lower equity and credit risk) than before to generate positive risk-adjusted returns in balanced portfolios. We believe that volatility will remain elevated in the near term as the global economy resets to a period of sub trend growth. However, lower starting valuations coupled with the benefits associated with the reopening of China’s economy, declining inflation, a peaking interest rate cycle and defensive positioning by market participants do provide the necessary backdrop for investors to look forward to a year of improved investment returns.

Asset allocation

We remain overweight South Africa, given attractive valuations across domestic equity, bonds and cash. In addition, we would expect that South African asset prices will also be supported by the reopening of China, which will likely improve risk appetite towards emerging markets while developed economies slow this year. During the quarter we increased the exposure to global fixed income whilst reducing the global equity exposure to underweight. The global economy is expected to decelerate sharply this year on the back of higher interest rates and further tightening in monetary policy. The risk is that central banks overtighten in their efforts to rein in inflation which has become their major concern. Higher interest rates will slow demand and banks willingness to extend credit as delinquencies increase. Many asset prices have already declined sharply, and the housing market has rolled over. Consumer and business confidence has deteriorated and as growth slows and consumers pull back on spending, unemployment is expected to deteriorate with knock on effects to the rest of the economy, as well as corporate profits. We have previously mentioned that global fixed income assets have once again become a viable investment option and are for the first time in over a decade providing attractive longer-term inflation adjusted returns. By increasing the exposure to global fixed income assets (particularly government bonds), multi asset portfolios will benefit from higher-for-longer yields and a degree of “protection” during this year’s expected slowdown in economic activity.

Domestic Equity – Overweight

The local equity market has performed reasonably over the past 12 months given how volatile the domestic and global economic and geopolitical backdrop has been. Loadshedding in South Africa intensified significantly during the year and together with a hawkish Reserve Bank and political uncertainty resulted in a derating of domestic shares that are exposed to the fortunes of South Africa. But attractive valuations relative to developed and other emerging markets provided an underpin to prices. Towards the end of the year, certain sectors such as luxury, resources and technology rerated from the improved news flow out of China. Consumer Staples were supported by the risk off trade and outperformed in line with global trends. Banking shares were well supported and benefitted from positive earnings surprises due to improved interest margins. Higher interest rates and an improvement in credit appetite from corporates and households, provided an underpin to the sector.The South African equity market is trading on depressed valuation multiples. Understandably given the global backdrop and that the world has entered the next downtrend in the global business and economic cycle. Although the South African economy will not be completely insulated from global economic and geopolitical developments, the country doesn’t face the same inflation challenges, which means that while higher interest rates will put the brakes on economic growth, the domestic economy is not expected to enter a recession as the interest rate “shock” to the economy will be less significant than developed economies where interest rates have been increasing at a very fast rate and from unprecedented low levels. Debt levels across households and corporates are still very much contained in South Africa and there are no signs of excesses and/or inflated valuations across asset classes in the economy. The medium-term outlook for earnings growth remains reasonable as companies continue to recover from the lows during the pandemic. We would expect volatility to continue in the near term until interest rates have peaked and/or global growth has stabilised. But given how attractive the local market is, we intend to stay the course by patiently staying slightly overweight the asset class while receiving attractive dividend cash flows in the meantime. Valuations do matter and we believe that patience will be rewarded, as it always does in the end.

Domestic Bonds - Overweight

In line with developments in the global bond market, South African bond yields have been trending lower during the last few months of the year, despite the uncertainty caused by the Phala Phala saga. This has resulted in positive performance from the asset class during 2022, and a very different outcome to the experience of developed market bonds. Attractive income yields (valuation) resulted in a significant outperformance of domestic bonds during the year, which has caused an outperformance of the SA All Bond Index relative to the Citigroup World Government Bond Index over 1, 3, 5 and 10 years. Government’s debt profile has surprised positively as government remained committed to prudent fiscal management and tax revenues have been much stronger than expected. A positive development which is likely to result in a lower rate of government bond issuances over the coming year, which will be supportive to bond valuations. International credit rating agencies have given SA the thumbs up by revising government’s sovereign credit rating outlook higher by one notch. Although it is too early to celebrate, it does signal an improvement in confidence towards SA and perhaps a lower risk premium in future. We believe that inflation has peaked, and the monetary policy tightening cycle is near its highest point. Given the cautious rhetoric emanating from the central bank we are of the view that the bank will hike rates by a further 50-75 basis points by mid-2023 before pausing. While we expect some level of volatility to persist, we believe the worst is behind us. The domestic fixed income market is not immune to developments in global bond markets but given the attractive starting income yields in both nominal and inflation adjusted terms, we would expect returns to be well above cash over the medium term, hence our overweight position to the asset class.

Global Equity – Underweight

The fortunes of risk asset prices such as equities are very much linked to the outlook for economic growth and, by implication, profit/earnings growth, which in turn is dependent on the trend of global liquidity and/or monetary policy. Central banks are quite correctly, on a mission to reduce inflation and inflation expectations which have remained stubbornly high despite recent declines in goods inflation. The concern for monetary authorities is that the longer inflation stays above target, the greater the risk that higher inflation becomes entrenched. The US Federal Reserve’s current assessment is that inflation risks are skewed to the upside, as non-housing related services inflation (55% of the US inflation basket) remains uncomfortably elevated. Part of the problem is that nominal wages have been increasing significantly on the back of an unusually robust and unbalanced employment market in which job openings substantially exceed supply of available workers leading to companies being forced to pay up for new hires and award material pay rises to existing employees in order to retain them. There appears to be a structural labour shortage. The participation rate (the percentage of the population that is either working or actively looking for work) is much lower than expected due to numerous factors, which include an accelerated retirement rate, increase in mortality rates due to COVID-19 and migration policies. In the US alone, it is estimated that the shortage in the labour market amounts to some 3.5 million employees, which means that it is unlikely that the unemployment rate will increase significantly, given that corporates (outside of the Information Technology sector) are hesitant to fire workers for fear that they will not be able to re-hire the necessary talent required in better times. In other words, corporates might be willing to sacrifice profit margins in the short term as demand slows to ensure that they are well positioned for the next upturn in the economic cycle. This poses a risk to the outlook for corporate profit growth (and in turn valuations of equities and corporate credit) as the global economy weakens, hence our lowering of equity risk in client portfolios.

Global Fixed Income – Underweight

We enter 2023 with markedly higher yields and whilst the global interest rate cycle is yet to reach its finale, bond markets will anticipate the peak well in advance and we see increasing evidence that this ‘topping out’ process for yields is already underway. We do not expect yields to fall sharply just yet, however, at current levels they look increasingly attractive on a medium to long-term horizon. With this in mind, we are poised to increase durations throughout our fixed income strategies although remain mindful that the mixed backdrop of slower growth yet persistently high inflation is likely to result in ongoing volatility in global bond markets. The Federal Reserve currently expects US interest rates to peak at just over 5% this year but this forecast may prove to be a little low based on the strength in the labour market and inflation. Whilst the lagged effects of tighter monetary policy are a clear headwind to the growth outlook, so far, the fully employed consumer has remained more resilient than expected. The US economy posted negative growth in the first half of the year, however, third quarter GDP rebounded to an above forecast +3.2% and indications suggest this positive momentum continued in the fourth quarter. We do expect economic growth to slow in the period ahead, but current evidence suggests that a deep and prolonged recession could be avoided, particularly if the interest rate cycle does stall at or around 5%. Inflation does appear to have passed its peak ensuring the bulk of monetary tightening is in the rear-view mirror, however, it still remains uncomfortably high necessitating additional interest rate hikes in the months ahead. Ongoing strength in the employment market and associated wage growth are complicating the outlook for inflation and whilst we do expect price pressures to continue to ease as we go through 2023, a rapid deceleration to central bank target levels in the 2% to 2.5% range is uncertain, at best.