Geopolitical uncertainty reclaims centre stage

As we close out the first quarter of 2026, it’s remarkable, almost astonishing, how dramatically the global investment landscape has shifted in just a matter of weeks. If we cast our minds back to early February, the prevailing tone across financial markets was one of growing optimism. Inflation was steadily trending lower across nearly all major economies, central banks were widely expected to begin cutting interest rates, and fiscal policy in countries such as the United States, Germany, and Japan was set to play a supportive role in sustaining growth. Positive corporate earnings revisions were broadening across many sectors in a way we had not seen for several years, and the rally in global equities was also being validated by improving fundamentals rather than sentiment alone.

Even emerging markets, which had endured a difficult few years, were beginning to outperform developed markets. A stable-to-weaker U.S. dollar, strong metal prices, and more favourable growth dynamics all supported a compelling narrative. In fact, heading into late February, the prospect that 2026 could be a year of synchronised global economic growth, with inflation and interest rates heading lower, was not only plausible but growingly shared among policymakers, economists, and investors alike.

the duration of the conflict will ultimately determine the impact on the global economy and financial markets.

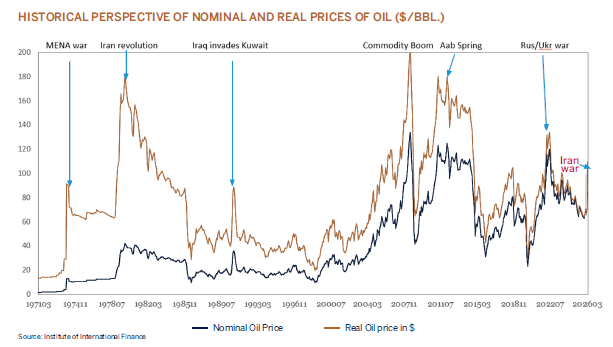

Yet this benign picture has quickly changed, and at a speed that leaves little question about the fragility of market expectations. The sudden and severe escalation of the war in Iran has disrupted global supply chains, sharply elevated geopolitical uncertainty, and, most critically, triggered a spike in oil & gas-related prices that has forced global financial markets to rapidly reassess the entire macroeconomic outlook - the duration of the conflict will ultimately determine the impact on the global economy and financial markets.

What began as a regional flare-up quickly evolved into a full-blown supply-side shock as the Strait of Hormuz, the world’s most important energy corridor, was effectively closed. Almost overnight, oil prices surged into triple-digit territory, and with that surge came the immediate repricing of inflation expectations, interest rate paths, and economic growth prospects. Up until a month ago, markets were positioning for further rate cuts to be sanctioned this year; today, they are struggling to determine whether central banks might instead be forced to raise rates again, or at best keep them unchanged through year end.

Certainly, the inflationary consequences of the spike in oil & gas prices prompted major bond markets to abandon any remaining probability of rate cuts this year. U.S. Treasury markets have rapidly repriced expectations for monetary policy and now lean toward the view that the Federal Reserve may have to keep interest rates unchanged for much longer than previously anticipated. Other central banks face even more difficult choices, especially the Bank of England and the European Central Bank, given the substantial vulnerability of their economies to higher energy prices.